Most lenders do not think about their AMC relationships as a strategy. They think about them as a vendor for selection to pick up a reliable company, sign an agreement, route the orders, and move on. That approach works until it doesn’t, and in 2026, the conditions under which it fails are more likely than at any point in recent memory.

UAD 3.6 mandatory adoption arriving November 2 means AMC readiness is no longer uniform across the market. Appraiser shortages in specific geographies create capacity constraints that a single AMC panel cannot always absorb. Loan type complexity, conventional, FHA, jumbo, rural, desktop, and hybrid increasingly demands specialization that one AMC may not provide equally well across all categories. And concentration risk, the exposure that comes from routing your entire appraisal pipeline through a single vendor, is a risk that regulatory examiners are paying closer attention to.

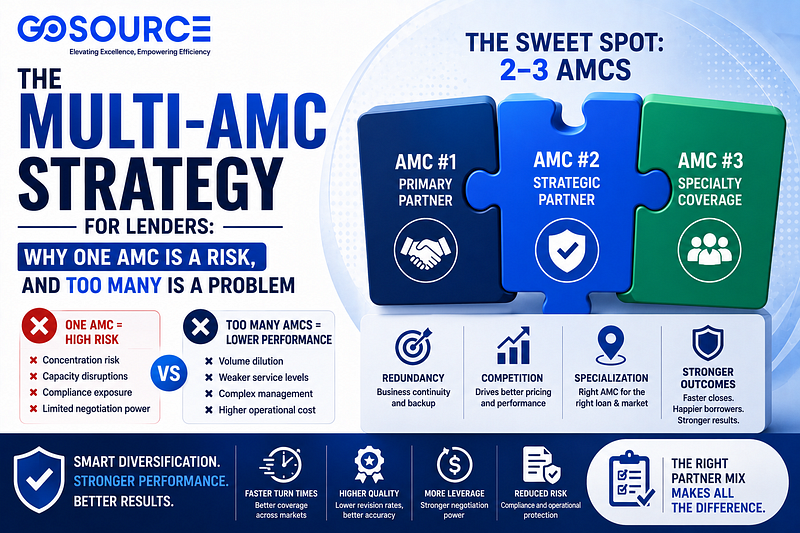

Most successful lenders maintain relationships with two to three AMCs. This provides coverage of redundancy, competitive pricing, and the ability to route different loan types or regions to the AMC best suited for each. A single-AMC strategy creates concentration risk, while too many AMCs dilute volume and weakens service levels.

That two-to-three number is not arbitrary; it reflects a real operational balance that this post will break down in full.

What AMC Concentration Risk Actually Means

Concentration risk is a term borrowed from portfolio management, and it applies to AMC relationships more directly than most lenders recognize.

When 100% of your appraisal orders flow through a single AMC, every operational or compliance failure at that AMC becomes your problem immediately, with no fallback. Consider the specific failure scenarios that concentration creates:

Capacity failure. A single AMC hit by an unexpected surge in order of volume, whether from a rate drop, a seasonal spike, or volume shifts from other lender clients, cannot always absorb the demand without turn time degradation. A lender with a single AMC relationship has no routing option when turn times start slipping. A lender with two or three has an immediate alternative.

UAD 3.6 readiness gaps. Not every AMC enters the November 2026 mandatory window equally prepared. The strongest lender-AMC partnerships in 2026 are no longer measured by volume alone; they are measured by closing rate impact, revision frequency, and time-to-final-report metrics. An AMC that is behind on UAD 3.6 platform integration, appraiser panel certification, or UCDP submission workflow becomes a pipeline risk for every lender routing volume through them with no mitigation option available to a lender who has no backup relationship in place.

Compliance exposure. Civil money penalties for appraiser independence violations can reach $10,000 per day for first violations and $20,000 per day for subsequent violations under CFPB Regulation Z § 1026.42. A single AMC compliance failure, an AIR breach, a documentation gap, a pattern of bias findings creates exposure across your entire pipeline if there is no alternative routing in place and no evidence of vendor diversification.

Geographic coverage gaps. No single AMC has equally deep active panel coverage in every market. An AMC with strong performance in metropolitan markets may have thin coverage in rural geographies, generating slow turn times and assignment cycling in exactly the markets where appraiser availability is already most constrained.

Why Too Many AMCs Creates Its Own Problems

The answer to concentration risk is not working with ten AMCs. Spreading volume too thin across too many vendor relationships creates a different set of problems that are just as damaging in practice.

Volume dilution weakens service levels. AMCs prioritize their highest-volume lender relationships for staffing, account management attention, and escalation of responsiveness. A lender sending thirty orders a month, split across eight AMCs, is a low-priority client at every one of them. A lender sending the same thirty orders split across two AMCs is a meaningful relationship at both, which translates directly into better service, faster escalation resolution, and more proactive communication.

Compliance oversight becomes unmanageable. Clear processes manage the number of AMCs in a lender roster, normalize expectations, and prevent a sharp rise in post-close findings due to uneven oversight. Lenders gain scale without sacrificing control. Managing vendor compliance documentation, performance review cadences, AIR audit trails, and UAD 3.6 readiness verification across ten AMC relationships simultaneously is a compliance burden that grows faster than the operational benefits justify.

Performance data loses comparability. One of the core benefits of a multi-AMC strategy is the ability to compare performance across vendors using the data from one relationship to benchmark the other and drive accountability. When volume is spread too thin, the data from each relationship is too sparse to be statistically meaningful. You cannot reliably compare revision rates between an AMC handling five orders a month and one handling fifty.

Onboarding and integration overhead multiplies. Every AMC relationship requires LOS integration, compliance documentation, SLA negotiation, and ongoing account management. Each additional relationship adds overhead that consumes operational capacity without proportionate return.

Building the Right Multi-AMC Structure

The two-to-three AMC model works because it captures the core benefits of diversification, coverage redundancy, competitive accountability, and specialization without the overhead and dilution that come from spreading volume too broadly. Here is how to structure it deliberately.

Designate a primary and secondary AMC, not equal.

Rather than splitting volume evenly, most lenders find that a primary-secondary structure performs better. The primary AMC receives the majority of volume, typically 60% to 75%, and carries the deepest integration, most developed account management relationship, and the strongest SLA accountability. The secondary AMC receives the remainder, serves as the coverage backup, and creates the competitive dynamic that keeps the primary relationship accountable.

This structure gives the primary AMC enough volume to treat the relationship as a priority while giving the lender genuine routing flexibility and a real alternative when performance slips.

Route by loan type and geography, not randomly.

A multi-AMC strategy becomes most valuable when routing logic is deliberate rather than arbitrary. Different AMCs genuinely have different strengths: deep rural panel coverage, FHA and government loan specialization, jumbo and non-QM experience, or specific state licensing depth. Mapping those strengths to your loan mix and routing accordingly extracts real performance value from the multi-AMC model, rather than treating it as a purely defensive play.

Use the relationship to drive competitive accountability.

One of the most underused benefits of working with two or three AMCs is the natural performance benchmark it creates. When you are tracking turn time, revision rates, escalation response, and UCDP acceptance rates across two relationships simultaneously, underperformance becomes visible immediately, and the existence of an alternative relationship gives the lender real leverage to demand improvement rather than simply accepting degraded service.

This only works if the performance data is actually tracked and reviewed. Build a monthly or quarterly performance review into every AMC relationship, using the same metrics across both, and share that data transparently with both partners. The accountability dynamic this creates is one of the most practical management tools available to a lender’s appraisal operations team.

Verify UAD 3.6 readiness for every AMC on your roster.

Heading into November 2026, every AMC in a lender’s roster should be verified for UAD 3.6 and MISMO 3.6 compatibility, not just the primary. An AMC serving as a backup or specialty routing partner that is not UAD 3.6 ready is not actually a functional backup after the mandate date. Readiness verification should include panel appraiser software certification status, UCDP submission testing documentation, and LOS integration compatibility confirmation.

What the Right AMC Mix Looks Like in Practice

For a mid-sized independent mortgage bank originating across multiple states, a well-structured multi-AMC model might look like this:

A primary AMC with strong nationwide panel coverage, confirmed UAD 3.6 readiness, full LOS integration, and an SLA commitment covering standard residential turn times in all active markets. This relationship handles the majority of conventional and conforming volumes.

A secondary AMC with demonstrated depth in rural geographies, FHA and USDA loan experience, and the panel coverage to absorb volume when the primary relationship hits capacity constraints in specific markets. This relationship also creates a competitive benchmark that keeps the primary accountable.

Together, these two relationships give the lender coverage redundancy, loan-type specialization, a real-time performance comparison, and genuine routing flexibility without the compliance overhead and volume dilution that comes from maintaining five or more vendor relationships simultaneously.

The Vendor Management Discipline That Makes It Work

A multi-AMC strategy is only as effective as the vendor management discipline behind it. The structural benefits of redundancy, accountability, and specialization only materialize if the relationships are actively managed rather than passively maintained.

This means documented SLA expectations with each AMC, real performance data tracked consistently across both, regular review cadences where that data is shared and discussed, and a clear routing protocol that both the lender’s operations team and both AMC partners understand. It also means maintaining the compliance documentation of AIR audit trails, UAD 3.6 readiness records, ROV process documentation for every AMC in the roster, not just the primary.

Lenders who treat their multi-AMC structure as a set-and-forget vendor arrangement do not capture the full benefit. Those who manage it actively using performance data, maintaining routing discipline, and holding both partners to documented benchmarks build an appraisal operation that is meaningfully more resilient and more competitive than either a single-AMC or a scattered multi-vendor model can produce.

How Go Source Valuation Supports Multi-AMC Lender Operations

At Go Source Valuation, we work with lenders and AMCs navigating the operational complexity that a multi-vendor appraisal strategy requires, from performance benchmarking support to UAD 3.6 readiness verification to back-office workflow management that keeps appraisal pipelines moving regardless of which AMC a given order routes through.

If you are building or restructuring your AMC vendor strategy for 2026, we would like to be part of that conversation. Visit our AMC Management Solutions page to learn more about how Go Source Valuation supports lender appraisal operations.

Frequently Asked Questions

What is a multi-AMC strategy for lenders?

A multi-AMC strategy is a deliberate approach to maintaining active relationships with more than one appraisal management company, typically two to three, to achieve coverage redundancy, competitive accountability, loan-type specialization, and protection against the concentration risk that comes with routing all appraisal volume through a single vendor.

How many AMCs should a lender work with?

Most successful lenders maintain relationships with two to three AMCs. This number captures the core benefits of diversification, redundancy, accountability, and specialization without the volume of dilution and compliance overhead that comes from spreading orders across too many vendors. A single-AMC relationship creates concentration risk; five or more AMCs have volume to the point where no individual relationship receives enough priority to perform at its best.

What is the AMC concentration risk?

AMC concentration risk is the operational and compliance exposure that results from routing all appraisal volume through a single vendor. When one AMC experiences capacity constraints, compliance failures, UAD 3.6 readiness gaps, or geographic coverage limitations, a lender with no alternative relationship has no routing option and absorbs the full impact of the AMC’s performance problems.

Should a lender split volume evenly between AMCs?

Not necessarily. A primary-secondary structure where the primary AMC receives 60% to 75% of the volume, and the secondary receives the remainder, often performs better than an even split. This structure gives the primary AMC enough volume to prioritize the relationship while still giving the lender genuine routing flexibility and a competitive benchmark.

How does a multi-AMC strategy improve performance accountability?

Working with two or three AMCs simultaneously creates a natural performance comparison. When turn times, revision rates, escalation response, and UCDP acceptance rates are tracked across multiple relationships using consistent metrics, underperformance becomes visible immediately, and the existence of an alternative routing option gives the lender real leverage to demand improvement.

Does UAD 3.6 affect the multi-AMC strategy?

Yes. Every AMC in a lender’s roster must be verified for UAD 3.6 and MISMO 3.6 compatibility before the November 2, 2026, mandatory deadline, not just the primary. An AMC that is not UAD 3.6 ready cannot serve as a functional backup or specialty routing partner after the mandate takes effect, making readiness verification a critical part of multi-AMC roster management heading into the second half of 2026.

What compliance documentation is required for each AMC on a multi-vendor roster?

Every AMC in the roster requires AIR compliance documentation, audit trail capability, UAD 3.6 readiness verification, and ROV process documentation, not just the primary relationship. Lenders carry vendor management responsibility for every AMC they work with, meaning compliance gaps at any vendor in the roster create exposure regardless of the volume that vendor handles.