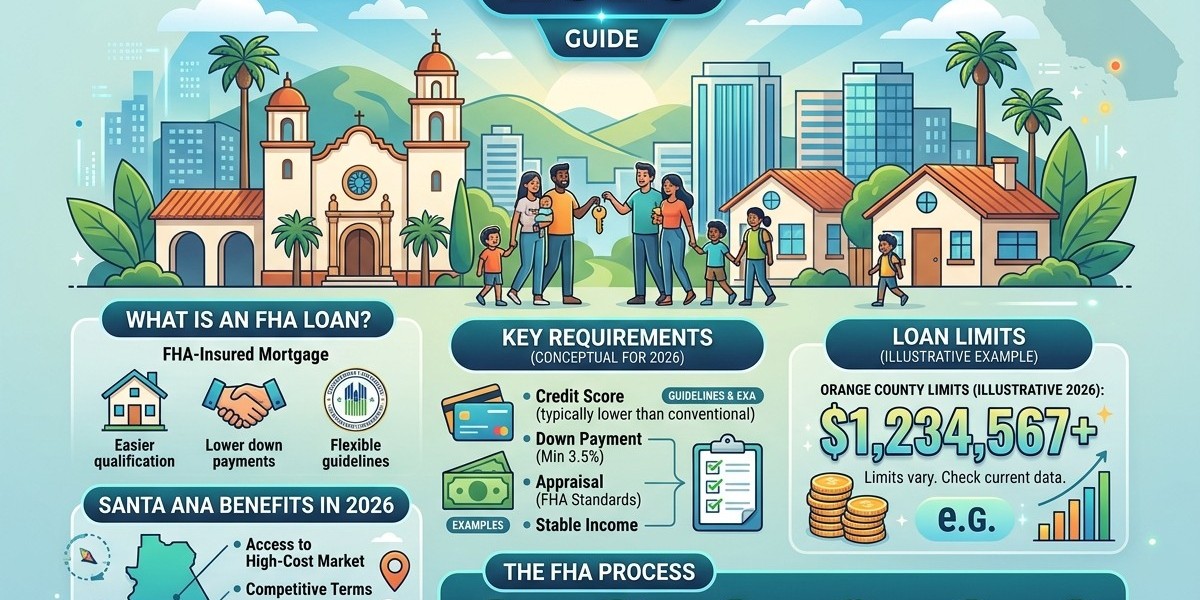

For many homebuyers in Santa Ana, the FHA loan is a highly accessible path to homeownership. Because Orange County is designated as a high-cost area, the FHA loan limits are significantly higher than the national baseline, providing strong purchasing power for local buyers.

2026 FHA Loan Limits in Santa Ana

Santa Ana is in Orange County, which falls into the "high-cost" category for FHA lending. As of 2026, the maximum FHA loan amount for a one-unit property is $1,249,125.

If you are interested in multi-unit properties (a strategy often used for "house hacking"), the limits are even higher:

| Property Type | 2026 FHA Loan Limit |

| Single-Family (1 Unit) | $1,249,125 |

| Duplex (2 Units) | $1,599,375 |

| Triplex (3 Units) | $1,933,200 |

| Fourplex (4 Units) | $2,402,625 |

Qualification Requirements

The FHA loan program is designed to be more flexible than conventional financing, particularly regarding credit and savings:

Credit Score:

580 or higher: You are eligible for the low 3.5% down payment.

500–579: You may qualify, but a 10% down payment is required.

Debt-to-Income (DTI) Ratio: Lenders generally prefer a DTI ratio of 43% or lower, though some lenders may approve higher ratios if you have "compensating factors."

Employment History: You must provide proof of stable employment and consistent income (typically for the last two years).

Primary Residence: The property must be your primary residence. You are required to move in within 60 days of closing and live there for at least one year.

Key Considerations

Mortgage Insurance Premium (MIP): Unlike conventional Private Mortgage Insurance (PMI), which can eventually be removed, FHA MIP is typically required for the life of the loan (unless you refinance). It includes an upfront premium and an annual premium paid monthly.

Property Standards: The home must meet strict HUD safety and livability standards. A certified FHA appraiser will inspect the property to ensure it is in good condition; if a home needs significant repairs, it may not qualify unless you use an FHA 203(k) loan for rehabilitation.

Investment Property Restrictions: You cannot use an FHA loan to buy a pure investment property. However, you can purchase a multi-unit property (up to 4 units) with an FHA loan, provided you live in one of the units as your primary residence.

Strategic Tips for Success

Get Pre-Approved: In a competitive market like Santa Ana, a pre-approval letter from an FHA-approved lender is essential to demonstrate your buying power.

Explore Down Payment Assistance (DPA): Look into California-specific programs like CalHFA, which can help with your down payment and closing costs.

Compare All Options: Even if you qualify for an FHA loan, it is worth comparing the total costs against a conventional loan. In some scenarios, if your credit profile is strong, a conventional loan might offer more favorable terms or lower long-term mortgage insurance costs.