Securing a mortgage is one of the most significant financial steps you will take when buying or refinancing a home. To find the right deal, you have to look past the initial advertised numbers and look closely at the relationship between competitive mortgage rates and upfront structural fees.

Finding a balance between your monthly interest charges and your immediate out-of-pocket settlement costs is the key to locking in an affordable, highly customized home loan.

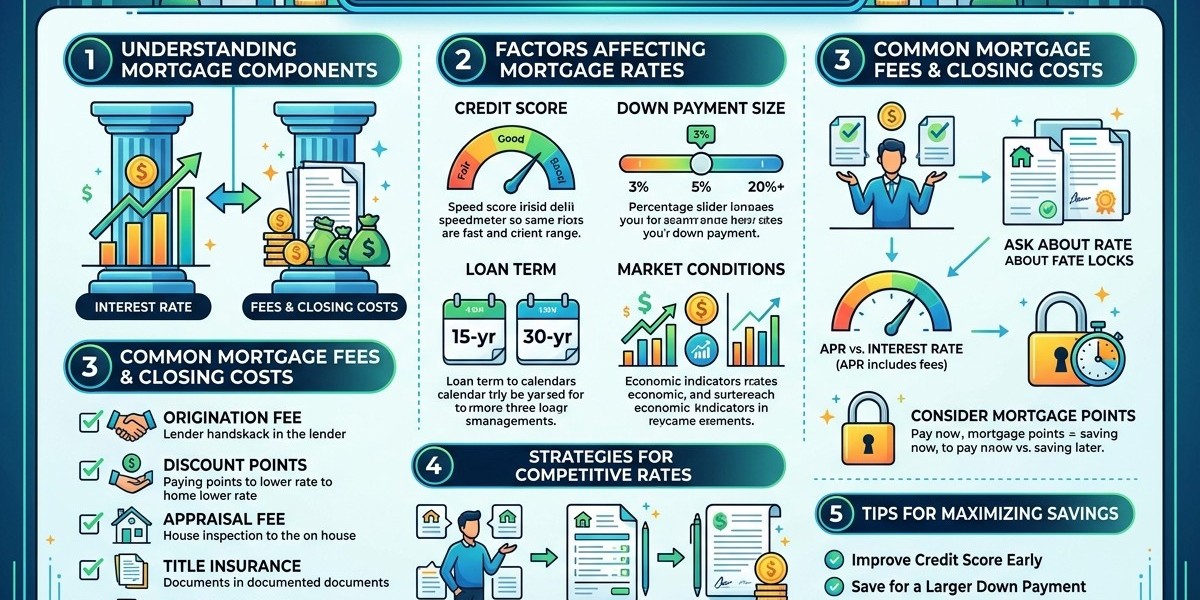

1. Navigating Current Market Interest Benchmarks

Mortgage interest rates fluctuate daily based on macroeconomic data, inflation reports, and Federal Reserve policy. Securing competitive mortgage rates depends heavily on your unique financial profile, including your debt-to-income (DTI) ratio, your employment history, and your down payment size. Lenders generally reserve their premium pricing for borrowers with a top-tier credit profile, typically a 740+ FICO score.

30-Year Fixed-Rate Mortgage: The most reliable option for long-term stability. It provides predictable monthly principal and interest payments for the entire 30-year lifespan of the loan.

15-Year Fixed-Rate Mortgage: Features a compressed amortization timeline. This option typically offers a lower interest rate than a 30-year loan, allowing you to pay off your home faster and save tens of thousands of dollars in total interest.

Adjustable-Rate Mortgages (ARM): Hybrid loans (such as a 7/1 or 5/1 ARM) that provide a lower, fixed introductory interest rate for a set number of years before adjusting annually based on current market benchmarks.

2. Breaking Down Upfront Mortgage Fees

Total closing fees typically amount to between 2% and 5% of your total loan balance. To secure low closing cost mortgages, you must carefully review your official Loan Estimate form to distinguish between standard administrative charges and negotiable lender fees.

Institutional Lender Fees

These are the administrative costs processed directly by your mortgage company to evaluate your file:

Loan Origination Fee: The core cost for processing, underwriting, and preparing your loan application. This is typically calculated as 0.5% to 1.0% of the total loan amount.

Application & Underwriting Fees: Flat processing fees ranging from $300 to $900 to cover internal risk assessment and background checks.

Independent Third-Party Fees

These are non-negotiable costs paid to external professional service providers required to finalize the real estate transaction:

Home Appraisal Fee: Typically costs $500 to $1,000 to verify that the property’s fair market value supports the contract purchase price.

Title Search & Title Insurance: Safeguards the transaction by confirming the real estate deed is entirely clear of historical liens, judgments, or ownership disputes.

Credit Report Fee: A small administrative charge (usually $35 to $80) to safely pull your records across credit repositories.

3. Strategies to Optimize Your Financing Structure

Achieving flexible mortgage options requires looking at how upfront cash outlays impact your long-term monthly savings. You can work with your loan officer to structure your closing costs using two main strategies:

Discount Points (Buying Down the Rate)

If you have extra cash at closing, you can choose to purchase mortgage discount points. One point generally costs 1% of the total loan amount and permanently lowers your market interest rate by roughly 0.25%. This strategy is financially ideal if you plan to keep the mortgage long enough to pass your break-even point.

Lender Credits (No-Closing-Cost Mortgages)

If you prefer to preserve your liquid cash, you can utilize lender credits. The lender agrees to pay your upfront closing costs in exchange for raising your permanent interest rate. This option keeps your upfront costs low but results in a higher monthly payment over the life of your loan.

Timeline for Securing Competitive Terms

To successfully lock in a competitive mortgage package, you should follow a clear, strategic path throughout your home buying journey:

Pro Tip for Borrowers: Keep your financial profile completely stable once your mortgage application is underway. To protect your final loan approval, do not take on new debt, open credit cards, move large unverified sums of money between accounts, or change your employment status before your loan officially funds.