Health insurance needs often evolve over time. A policy that seemed suitable a few years ago may no longer provide adequate coverage, sufficient hospital network access, or the features required to address changing healthcare priorities. As medical costs continue to rise across India, policyholders increasingly seek better coverage options without sacrificing the benefits they have already accumulated.

This is where health insurance portability becomes important. Portability allows individuals to switch from one insurer to another while retaining specific continuity benefits earned under their existing policy. When done correctly, porting can help policyholders access improved coverage while preserving valuable advantages such as waiting period credits.

Understanding how portability works is essential for anyone looking for the best health insurance policy in India without losing hard-earned policy benefits.

What Is Health Insurance Portability?

Health insurance portability refers to the process of transferring an existing health insurance policy from one insurer to another while retaining certain continuity benefits as permitted under applicable regulations.

The concept was introduced to enhance consumer choice and encourage insurers to maintain high service standards.

Portability enables policyholders to:

Switch insurers

Upgrade coverage options

Access improved features

Explore broader hospital networks

Retain eligible waiting period credits

The ability to move to a new insurer without starting completely from scratch has made portability a valuable feature for policyholders seeking better healthcare protection.

Why Do People Port Their Health Insurance Policies?

Several factors may motivate a policyholder to consider portability.

Better Coverage Options

Healthcare needs often increase with age and family responsibilities.

A policy purchased years earlier may no longer provide adequate protection against modern healthcare costs.

Enhanced Benefits

Many policyholders seek plans offering:

Higher sum insured

Wellness benefits

Digital healthcare services

Expanded treatment coverage

Improved customer support

Larger Hospital Networks

Access to a wider network of hospitals can improve treatment convenience and reduce out-of-pocket expenses.

Improved Claim Experience

Customer service and claims efficiency frequently influence portability decisions.

Individuals searching for the Best Health Insurance Policy In India often evaluate insurers based on both product features and service quality.

Benefits That Can Be Retained During Portability

One of the biggest concerns policyholders have is whether existing benefits will be lost after switching insurers.

Fortunately, portability provisions help preserve certain continuity advantages.

Waiting Period Credits

The most important portability benefit is the transfer of waiting period credits.

This may include waiting periods already served for:

Pre-existing diseases

Specific illnesses

Certain medical procedures

For example, if a policyholder has already completed three years of a four-year waiting period for a pre-existing condition, the completed period may be credited under the new policy, subject to applicable portability rules.

Continuous Coverage Benefits

Maintaining uninterrupted coverage helps preserve policy continuity.

This continuity can play an important role in long-term healthcare planning.

Accumulated Insurance History

A consistent insurance record often strengthens a policyholder's position during the portability assessment process.

Benefits That May Not Transfer Completely

While portability offers significant advantages, not every policy feature automatically transfers.

Policyholders should carefully review:

Product-specific benefits

Wellness rewards

Loyalty bonuses

Special add-on features

Unique policy conditions

Certain benefits may differ between insurers because products are structured differently.

Before initiating portability, compare the proposed policy carefully to understand any changes in coverage.

When Is the Right Time to Port a Policy?

Timing plays a crucial role in successful portability.

During Renewal

Portability is generally initiated around the policy renewal period.

Starting the process early provides sufficient time for documentation, underwriting, and approval.

Before Coverage Needs Change Significantly

Many policyholders wait until they are dissatisfied with their existing policy.

However, portability decisions are often more effective when made proactively rather than reactively.

When Better Alternatives Become Available

The health insurance market evolves continuously.

New products frequently introduce enhanced benefits, making periodic policy reviews worthwhile.

Those evaluating the Best Health Insurance Policy In India should regularly assess whether their existing coverage still aligns with their healthcare needs.

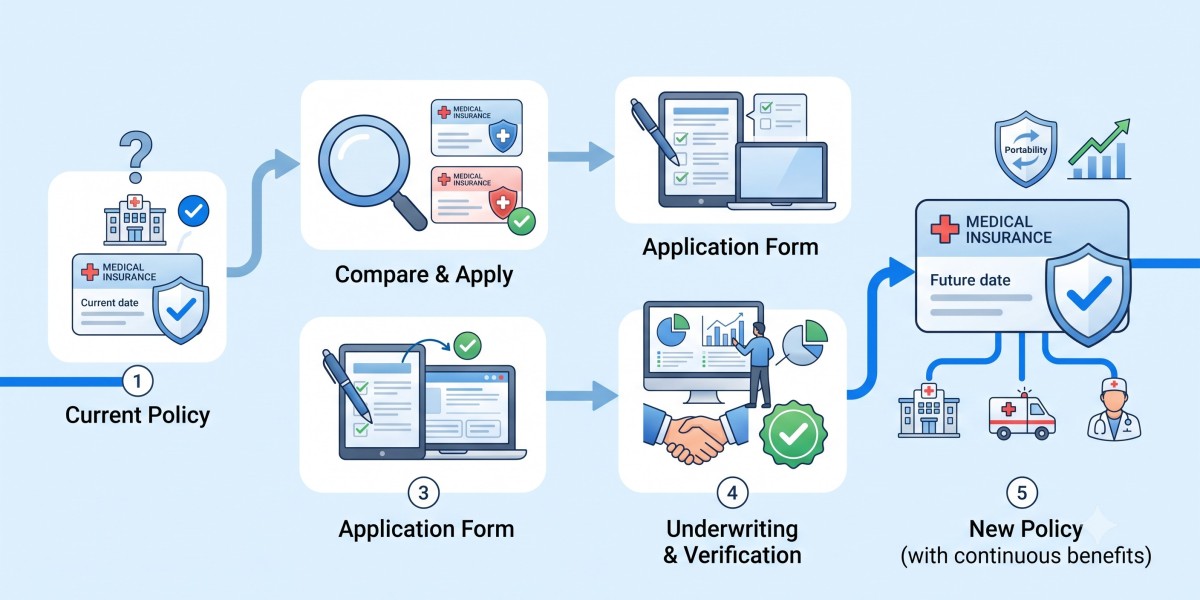

Step-by-Step Guide to Porting Your Health Insurance Policy

Step 1: Assess Your Current Policy

Before switching, evaluate:

Current sum insured

Existing benefits

Waiting period status

Hospital network access

Claim history

Understanding what you already have helps identify meaningful improvements.

Step 2: Compare Available Options

Look beyond premium costs.

Evaluate:

Coverage scope

Exclusions

Network hospitals

Claim settlement processes

Additional healthcare benefits

A lower premium does not always translate into better value.

Step 3: Apply Within the Required Timeline

Portability requests should generally be initiated well before policy renewal.

Starting early allows sufficient time for processing and reduces the risk of coverage gaps.

Step 4: Submit Required Documentation

Commonly required documents may include:

Existing policy documents

Renewal notices

Identity proof

Medical declarations

Claims history information

Accurate documentation helps streamline the evaluation process.

Step 5: Underwriting Assessment

The new insurer will review:

Age

Medical history

Existing conditions

Claims experience

Coverage requirements

Portability does not eliminate underwriting evaluation.

Insurers retain the right to assess risk before issuing a policy.

Step 6: Receive Approval and Complete the Transfer

Once approved, the new policy becomes active according to the agreed terms.

Policyholders should carefully review all policy documents before finalising the transition.

Common Mistakes to Avoid During Portability

Focusing Only on Premium Costs

Choosing a policy solely because it is cheaper can result in reduced coverage quality.

Ignoring Exclusions

Every policy contains exclusions that may affect claim eligibility.

Reviewing these provisions is essential.

Delaying the Process

Waiting until the last moment may create unnecessary pressure and increase the risk of administrative complications.

Overlooking Hospital Network Availability

A strong hospital network can significantly improve access to quality healthcare services.

Failing to Compare Benefits Thoroughly

Coverage enhancements should justify the switch.

Policyholders should ensure that the new policy genuinely represents an improvement over the existing one.

How Portability Supports Better Healthcare Planning

Portability encourages insurers to improve products and services while giving consumers greater flexibility.

This benefits policyholders by enabling them to:

Adapt coverage to changing needs

Access enhanced healthcare solutions

Improve financial protection

Maintain continuity benefits

The ability to switch providers without losing waiting period credits empowers consumers to make more informed healthcare decisions while choosing the right health insurance policy for their evolving needs.

A similar principle of continuity can be observed in Insert Insurance Type insurance, where preserving accumulated benefits often plays an important role in long-term policy value.

Important Factors to Evaluate Before Porting

Before making a final decision, consider the following:

Sum Insured Adequacy

Medical inflation continues to increase treatment costs across India.

Ensure the proposed coverage amount aligns with future healthcare needs.

Waiting Period Structure

Confirm how waiting period credits will be recognised under the new policy.

Claim Settlement Experience

Efficient claims support can significantly influence policyholder satisfaction.

Product Features

Look for benefits that support both preventive care and hospitalisation coverage.

Long-Term Suitability

Portability should be viewed as a long-term healthcare decision rather than a short-term financial adjustment.

Individuals searching for the Best Health Insurance Policy In India should prioritise sustainable value rather than temporary cost savings.

The Growing Importance of Portability in India

As consumer awareness increases, portability has become an increasingly valuable feature within India's health insurance ecosystem.

Policyholders are no longer limited to a single insurer for life. Instead, they have the flexibility to pursue better coverage options while preserving key continuity benefits.

Many insurers, including Niva Bupa, recognise the growing demand for portability and have developed processes that support smoother transitions for eligible policyholders.

This flexibility strengthens competition and ultimately benefits consumers through improved products and services.

Conclusion

Health insurance portability offers policyholders an opportunity to upgrade their coverage, access better healthcare benefits, and improve overall financial protection without sacrificing important continuity advantages. When managed correctly, portability can preserve waiting period credits and help maintain long-term coverage value.

The key to a successful transition lies in careful planning, timely application, and thorough comparison of available options. By understanding how portability works and evaluating policies beyond premium costs alone, consumers can make informed decisions that support their evolving healthcare needs.

For anyone seeking the Best Health Insurance Policy In India, portability provides a valuable pathway to better coverage while retaining the benefits earned through years of responsible policy ownership. The Best Health Insurance Policy In India is ultimately one that balances comprehensive protection, long-term value, and continuity of benefits for both present and future healthcare needs.